The Charging Station - No. 26

The Charging Station - No. 26

Carbon Adjusted-Cost-of Capital

Hey friends,

We’re back after taking the last few weeks off to regroup.

I picked this week to start publishing again because the content in the energy sector has been incredibly strong over the last 10-14 days.

After running a few polls on social media and thinking about the direction I want to take the newsletter moving forward, I’ll be posting some longer-form content. Most of it will be original and I will still be including curated links at the bottom, they just won’t be as prominent.

Hopefully, you’ll find the change to be a positive one and enjoy the newsletter more than ever. Please send feel free to send over any feedback - it is appreciated and helpful.

With that out of the way, let’s get to it.

The Climate-Cost-of Capital

A small, but growing, subset of investors are increasing the importance of firm-specific ESG behavior in their investment criteria. This year, financial behemoths like Blackrock and Goldman Sachs announced they would be considering sustainability metrics in all of their allocation decisions.

Yet, most investors are still hesitant to integrate environmental factors into their processes because they aren't quite sure how, or if, they align with their traditional financial objectives.

Studies have shown that as recently as 2019, a majority of fiduciaries continue to assume that adding ESG issues into their process could potentially lead to suboptimal alpha. Investors still in large part do not closely monitor decarbonization efforts directly, and you can’t manage what you don’t measure.

The primary reason for this lack of interest in ESG is not due to apathy, but instead to the fact that connecting a company's ESG behaviors to financial return remains extremely difficult to do in a standardized way.

To activate the large-scale capital currently sitting on the sidelines and needed for a transition to a more climate-resistant economy, it is vital that institutional investors can align their portfolio returns with sustainability metrics so that the cost-of-capital will follow along.

That process is in its early stages but is underway. In the first quarter of 2020, ESG capital inflows surpassed 2017 + 2018 combined, and sustainable debt instruments are up 100x since 2012 for a total of $465B in 2019.

The former numbers should be viewed with some skepticism since ESG has become so broad that it is now hard to define. Most big tech companies fit under the ESG umbrella, but it’s not exactly clear how ESG correlates to their return when controlled for other macro factors.

For example, Alphabet’s stock is up almost 200% since 2015 but it is impossible to define how much, if any, of that increase can be attributed to ESG factors even though they’ve substantially reduced their carbon footprint in the last five years — therein lies the problem.

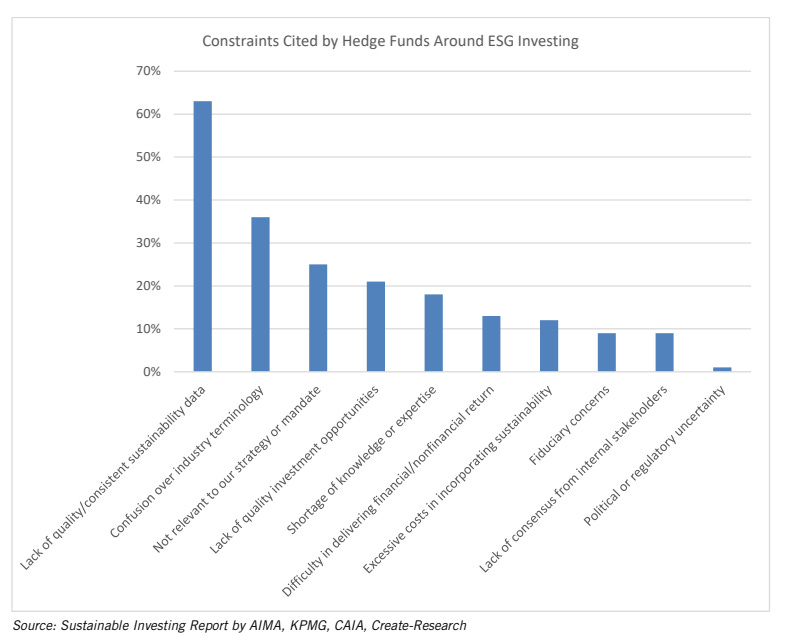

While ESG metrics and frameworks are widely available, most hover around .61 correlation to returns and by contrast credit ratings are .98 or higher. This discrepancy highlights the need for standardized metrics that are less “noisy”.

There is a growing consensus that climate and carbon are the ripest for clarity and standardization as evidenced by the growing number of frameworks and public commitments. Additionally, as I mentioned above, financial markets are beginning to demand reports from companies directly instead of through 3rd parties.

Since C-Suite compensation is often tied to equity value, and the market forces above are pushing companies to take on environmental challenges themselves - without waiting on regulators. For example, both Starbucks and Microsoft announced major sustainability initiatives earlier this year. In a surprising move, some oil and gas companies have done the same.

Additionally, most reports so far have focused on DOES it pay to be green, but as more enterprises take on ambitious climate goals we will have the data to understand WHEN it pays to be green. It is then and only then can we accelerate the adoption of the most effective decarbonization processes.

Moving forward, these plans will and must come under more scrutiny, and it’s vitally important we consider factors like:

Revenue-adjusted emissions (revenue: GHG emissions)

Does the intention match the result? Is it repeatable?

Are the goals aggressive enough to beat industry standards and tied to timelines that allow for accountability?

Can the processes be tied directly to issues (accounting transparency, governance, etc..) we know directly correlate to return?

Empirically connecting risk-adjusted returns, and subsequently, cost-of-capital and enterprise values to sustainability is an important next step in reducing the carbon intensity of the economy.

Worth Your Time

1.

“We have left the era where a company’s “values” are fully disconnected from their valuation. Issues like climate are directly impacting business decisions, capital allocation, and asset valuation. We believe ESG and sustainability will be the dominant investment trend for the coming decade, as passive investing was for the last.”

The convergence of the cost of capital and sustainability is one of the most important secular trends in climate tech. However, a lack of robust, standard data sets for financial reporting prevents “impact” from being measured consistently across sectors. You can’t manage what you don’t measure which creates big opportunities in data reporting and transparency.

— The Great Divorce: Is it time for E, S, and G to Part Ways?

2.

“Like the current pandemic it (climate change) will require a large amount of data and analysis to understand, but the slower pace means that more effort needs to be spent on deciding which data will be most useful in planning a strategic response.”

The nature of energy and industry is that they both run tangent to almost every sector, making data fragmented and hard to find. That makes this report from BNEF essential for anyone thinking about energy, agriculture, industry, and climate.

3.

“Allowing utilities to claim 80% of cloud expenses as capital investments simplifies that process without placing onerous burdens on providers.

The proposed revisions add clarity, will streamline the administration of the proposed rule, and will further promote additional benefits to customers, harnessing the flexibility, efficiency, and scalability of cloud-based solutions”

— Illinois advances pioneering proposal for utility rate recovery of cloud computing investments

A potential game-changer for startups chasing utilities as customers. If adopted, the model would set a standard that could lift the largest regulatory hurdle currently preventing utilities from adopting new software products.

What I’m Thinking About

Consistency and scalable learning to create processes that lead to better decisions.

See you next weekend,

Kevin

Did your brilliant friend send you here?